Income Tax Filing Explained: What Determines My Tax Bill?

No one likes having to file taxes. For the majority of US citizens, tax filing is something to dread. We try to put off for as long as possible, right up until the April 15th deadline.

Table of Contents

No one likes having to file taxes. For the majority of US citizens, tax filing is something to dread. We try to put off for as long as possible, right up until the April 15th deadline.

Part of the fear around taxes is not knowing whether we’ll owe Uncle Sam money until the day we file. The big question is: what determines how much money you’ll owe the IRS? Or, if the math is on your side, how much money will the government owe you?

At the most basic level, what you owe or receive as a refund is simply the difference between what you should have paid over the course of the previous year and what you actually paid.

What you owe and what you have paid can differ for a number of reasons. Choosing the wrong number of allowances on your W-4, investment sales that aren’t taxed at the time of the sale, and bonuses or other unusual, one-time payments are all ways that these numbers might become uneven.

You can easily check your records and pay stubs to see what you paid in taxes last year. But how do you calculate what you should have paid? We’ve broken it down so that you can better understand what factors are contributing to your owed taxes. In what follows, we’ll break down everything you need to know about your tax filing status, income tax brackets, ordinary income vs long-term capital gains, deductibles and tax credits, owing the IRS money, and doing the self-employed 1099 tax thing.

Ordinary Income vs Long-Term Capital Gains

Let’s start with defining your different sources of income. There are two types of income you need to worry about: ordinary income and long-term capital gain income.

Your ordinary income is the money that the government is going to take a cut of for your taxes. Generally, any money you earn as compensation for work is considered ordinary income. For the average taxpayer, this includes any and all of the following:

- Hourly wages

- Salaries

- Tips

- Commissions,

- Interest income from bonds

- Income earned from a business

- Some rents and royalties

- Short-term capital gains held for less than a year

- Unqualified dividends.

Any money that you make off of these sources is subjected to the marginal tax rate scheme we detailed above.

Great. But is all of your income subject to the marginal tax scheme? The answer is mostly. But there are some exceptions.

If you own investments or assets (i.e., stocks, real estate) for longer than a year, any profit you make off of them is considered long-term capital gains. There are also certain dividends that fall under this category, called “qualified dividends.” Long-term capital gain income is taxed differently than ordinary income, at a favorable capital gains rate of 0%, 15% or 20%, depending on your income level.

What’s important to note is that the long-term capital gains tax rate is significantly lower than the ordinary income tax rate for all income levels. As a result, you get to keep more of your money made from long-term capital gains than from ordinary income. This is why investor billionaire Warren Buffett has been quoted saying that he pays a smaller tax rate than his secretary. He pays a long-term capital gains tax, while she has to pay the ordinary income rates. But that’s a topic for another day.

Identifying Your Tax Filing Status

When it comes time to file your tax return, you’ll have to select one of five tax filing statuses. This will determine the rate at which your income is taxed. Your tax filing status is important since it determines your standard deduction and the tax brackets (and therefore tax rates) you are subject to. The different categories of tax filing status are:

Single – You’re single if on the last day of the year you are unmarried or legally separated from your spouse under a divorce or separate maintenance decree and you do not qualify for another filing status.

Married Filing Jointly – Married couples can choose to file a single joint return that includes the combined income of both spouses and combined deductions of allowable expenses.

Married Filing Separately – Married couples who do not choose to file taxes jointly must choose this tax filing status. Spouses choose this method if they want to be responsible for only their own tax, or determine they can reduce their tax liability greater than if filing jointly.

Head of Household – You can select this status if you are unmarried or considered unmarried on the last day of the year. And you paid more than half the cost of keeping up a home for the year. And a qualifying child or qualifying relative lived with you in the home for more than half the year, (except for temporary absences such as school). However, the IRS gives a qualifying parent a pass and does not have to live with you.

Qualifying Widow(er) with Dependent Child – If your spouse died during the tax year in question and you have a qualifying child who lives in the home with you, then you can choose this tax filing status which entitles you to use the Married Filing Jointly tax rates and the highest standard deduction amount (if you do not itemize deductions).

Based on your tax filing status, the IRS will apply a specific tax brackets to your ordinary income. This might feel confusing at first, but let’s break it down to simplify it.

When you file taxes for the 2019 tax year, the IRS will apply up to seven tax rates to your taxable ordinary income – 10%, 12%, 22%, 24%, 32%, 35%, 37%. In the US, we have a progressive tax system: the more money you earn, the bigger the tax rate you’ll be subjected to: 10% being the lowest, 37% being the highest.

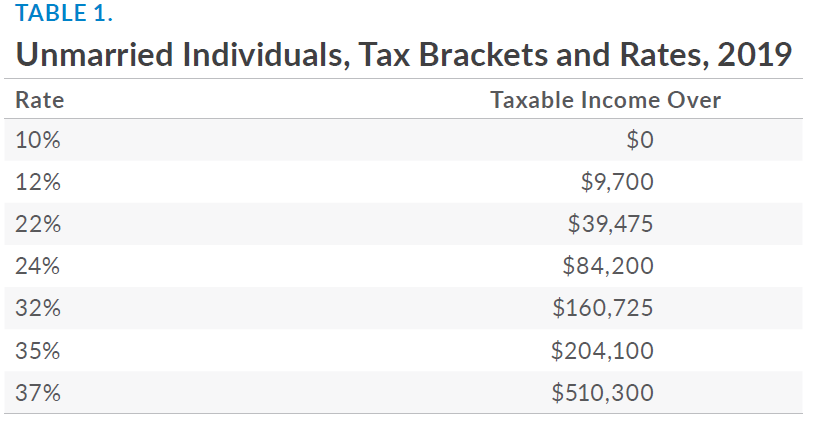

Does this mean that a high earner will pay 37% of their income to taxes? No, not entirely. The IRS uses something called marginal tax rates, which means that each tier of your income is taxed differently. For example, for the tax year 2019, an individual taxpayer who selects the Single tax filing status will be subjected to the following ordinary income bracket:

The way the marginal tax rates work:

- The first $9,700 of ordinary income that any Single tax filer reports will be taxed at 10%.

- If you report more than $9,700 in income, then the amount between $9,701 to $39,475 is taxed at 12%.

- If you report more than $39,475, then the amount between $39,476 to $84,200 is taxed at 22%.

This process continues with the tax rate escalating on any earnings beyond the upper amount for any given rate. At the extreme, if you’re lucky enough to earn greater than $510,300, all earnings in excess of $510,300 will be taxed at 37%.

Let’s look at a scenario for a Single tax filer: Suppose you report $9,800 in ordinary income, how much tax do you owe? Well, the first $9,700 is taxed at 10% so you owe $970 to start. Then the next $100 of your ordinary income is taxed at 12% so you owe another $12. $970 + $12 = $982. See, it’s not too hard to grasp once you understand how tax income brackets work.

Let’s take another example of a Single tax filer: Suppose you have a nice round $40,000 in ordinary income. To calculate how much you owe, start with your bottom bracket and work your way up. Again, the first $9,700 is taxed at 10% so you owe $970 to start. Then the amount between $9,701 to $39,475, which in this case amounts to $29,774, is taxed at 12%, so you owe another $29,774 x 0.12, or $3572.88. Then the amount between $39,476 and $40,000–just $524–is taxed at the next tax rate of 22%, so you owe another $524 x 0.22 or $115.28. Your final tax bill is $970 + $3572.88 + $115.28 = $4658.16.

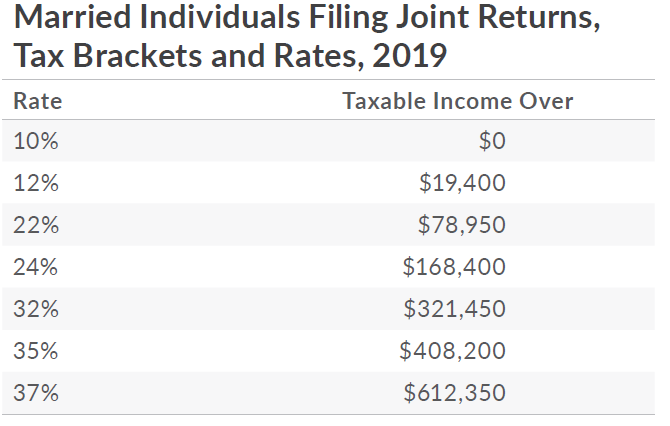

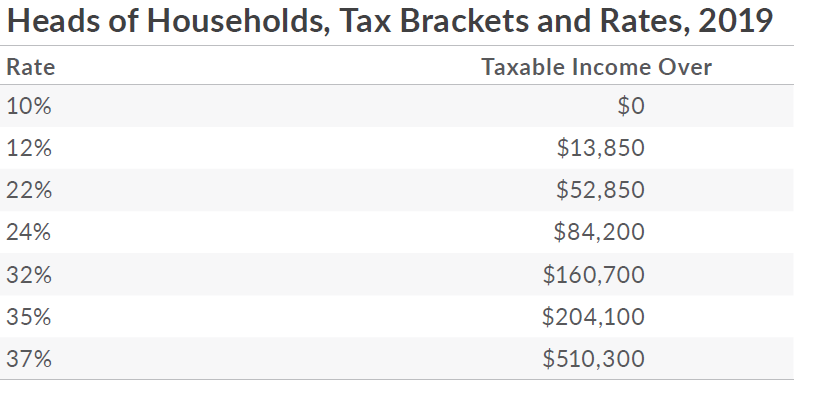

Now that you know how tax rates are calculated, you should understand that the tax brackets (i.e. the chart which determines the marginal rates applied to different incomes) are slightly different for each tax filing status. We included the single tax filing bracket above. See below for the two other most common tax brackets – the Married Filing Jointly tax bracket and the Head of Household tax bracket:

You can see that the Married Filing Jointly tax brackets is generally the most favorable of the tax brackets (since the higher tax rates don’t kick in until a higher income level). The Head of Households tax bracket is also slightly more favorable than the Single tax filing bracket.

Making the Most of Your Tax Deductions

Say you’re a Single individual tax filer with a nice career at a company that pays you a salary of $90,000 a year. It’s good money, but for the 2019 tax year you’re going to get hit with the 10%, 12%, 22%, and 24% marginal tax rates. Luckily, there is something you can do to lower your ordinary tax income so the full $90K isn’t subjected to tax. It’s called a tax deduction.

A tax deduction is when you itemize something that you’ve spent money on in that last year–this can be anything that falls under the IRS’s qualifications–and subtract that amount from your ordinary income. When you do your taxes, then, you’ll be working with a lower ordinary income, and thus pay less in your taxes.

If you’re the $90K individual in our example, the IRS lists over 20 deductions (charitable contributions, medical and dental expenses, student loan interest, etc.) that you can itemize on your tax return to lower your ordinary income from $90K to, let’s say, $80K.

But itemizing can be a pain for both you the tax filer and the IRS, so to make life simpler for everyone, Uncle Sam also gives us all the option of taking a standard deduction. Your standard deduction amount is determined by your filing status.

For tax year 2019:

- The standard deduction for a Single filer is $12,200

- For Married – Filing Jointly or Widow(er) with Dependent Child it’s $24,000

- For Married – Filing Separately it’s $12,200

- For Head of Household it’s $18,350

In our example, a Single individual tax filer making $90K can choose the standard deduction to reduce their ordinary income subject to tax by $12,200 to $77,800.

If you take the standard deduction, then you can’t also itemize your deductions–it’s one or the other. If you have less than $12,200 of qualifying deductions to itemize, then you should absolutely take the standard deduction as it’s practically free money, plus it’ll save you time.

However, if you have more than $12,200 in qualifying deductions and want to lower your taxable income even further, you should itemize your deductions. Itemizing requires you to list each deduction. We highly recommend that you maintain records of these deductions in case the IRS decides to audit you.

You should also keep in mind that unusual or unrealistic itemized deductions are what catch Uncle Sam’s eye and can trigger an audit. If you’re risk-averse or maybe don’t have all the documents to back up even legitimate deductions you’re entitled to, then you can always just take the standard deduction and call it a day.

Getting Those Tax Credits

Another way the IRS allows taxpayers to hang on to a bit more money is through tax credits. Tax credits are exactly what they sound like–credits that the IRS grants to qualifying individuals that directly lower how much they owe the IRS. This is different than deductions, which only lower your ordinary income subject to the marginal tax rates.

The most common tax credit is the Child Tax Credit (CTC). For the 2019 tax year, the CTC is up to $2,000 per qualifying child. A qualifying child is a US citizen age 16 or younger at the end of the calendar year, can be claimed as a dependent, and lives with the taxpayer for more than six months of the year. However, the CTC phases out at $200,000 of modified adjusted gross income, or $400,000 for married couples filing jointly, so if you’re a higher earner you won’t be able to claim the credit.

Suppose you’re Married – Filing Jointly with three kids and as you complete your tax return you find that you owe the IRS $5,000. If you qualify for the $2,000 CTC for each of the three children ($6,000 total), then because the credit applies directly to your liability, the IRS now owes you a cool $1,000 ($6,000 in total credits minus your $5,000 tax bill) as up to $1,400 of the credit is refundable for each qualifying child. Pretty sweet.

The IRS lists a number of credits for individual taxpayers that can be used to lower your tax bill if eligible, but unlike the CTC, many of them are nonrefundable. For example, the 2019 Federal Adoption Credit of $14,080 is given to offset the cost of adopting a child. But it is nonrefundable, which means that if you owe the IRS $5,000 and then apply a qualifying Federal Adoption Credit, your tax bill simply drops to $0 and you aren’t given the difference of $9,080 as a refund. Still, you should claim as many credits as you can since these directly lower the taxes you owe Uncle Sam.

So Why Might I Owe the IRS Money?

Now that you’re familiar with the basics of tax filing, you may be asking why you have to send Uncle Sam *more* money after you file your return. If you are being told that you still need to pay, you probably underpaid your taxes last year. There are a couple of reasons that this could have happened.

Tax Withholding

According to the IRS, your employer will withhold income tax from your paycheck and send it straight to the IRS in your name. The withheld amount is determined by the Form W-4 you fill out at the start of employment. W-4’s give you the opportunity to claim allowances, and each allowance you use means less money gets sent straight to the IRS, and more of your wages/salary appear in your paycheck. If you, ahem, overestimated those allowances, you may owe Uncle Sam some cash money.

To avoid this senario, all you have to do is complete a new W-4, clarifying to your employer that you do not want to withhold this money any more. The IRS offers a handy tax withholding estimator tool you can use when completing Form W-4 so that you don’t wind up with too much or too little federal income tax withheld. Keep in mind that if you withhold too few taxes and end up owing the government money, then you might also be faced with interest and penalties.

Sale of Investments or Assets

If you’ve made some money by finally cashing in those stocks your grandparents gave you, dabbling in daytrading, or selling a piece of fine art or real estate, then, by law, Uncle Sam is entitled to a cut of the profits. Remember those long term capital gains we talked about? Yeah, those apply here.

As discussed, the capital gains tax rate is determined by your tax filing status, taxable income, and whether the asset was held for more than a year. If you didn’t send in a tax payment when you made the sale, you’ll have to pay when you file, decreasing your overall refund or possibly pushing you into the cash-owing, check-writing zone.

The good news is that this works both ways! If you lost money selling an asset or investment, then you can deduct up to $3,000 of net capital losses from your ordinary income to lower your tax bill. If your net capital loss is more than this limit, you can carry it forward to later years to lower future tax bills.

Additional Income

Capital gains isn’t the only source of additional income that will increase your tax liability. If you received a refund from the state during the tax year then you’ll likely owe a portion of it to the IRS. If you received unemployment benefits then that too is taxed by the federal government. And if you’re self-employed or made extra cash off your side hustle and didn’t send the IRS an estimated tax payment, then you’ll have to pay up big time when you file your annual return.

Help! I’m Self-Employed and Can’t Figure Out This Tax Thing

Having an employer makes things much easier when it comes to tax filing because they automatically deduct taxes from your paycheck and send it to the government.

When you work for yourself, you’re responsible for settling up with Uncle Sam each quarter, and it’s not always straightforward because you have to pay an income tax and a self-employment tax.

The Self-Employed Income Tax

Let’s start with the basics: the income tax. You’re making bank as a freelancer, so after you deduct certain qualifying business expenses, you’re left with an amount of money that will be treated as ordinary income and subject to the seven tax brackets. The IRS requires you to send in an estimated tax each quarter. Those due dates are as follows:

1st payment: April 15, 2019

2nd payment: June 17, 2019

3rd payment: Sept. 16, 2019

4th payment: Jan. 15, 2020*

* You don’t have to make the payment due January 15, 2020 if you file your 2019 tax return by January 31, 2020, and pay the entire balance due with your return.

You can use Form 1040-ES to estimate your quarterly income taxes and pay online. With the proliferation of the gig economy, a lot of taxpayers are raking in extra cash on the side but failing to file quarterly tax payments resulting in sticker shock tax bills along with interest and fines.

Self-Employment Tax

The Self-Employment tax is the biggie that most people don’t realize exists until it’s too late.

When you work for an employer, the company must pay into Social Security and Medicare on your behalf. It’s typically known as a payroll tax and completely different than the income tax we’ve been discussing up until now. If you work for yourself, then not only do you have to pay the income tax, it’s you who has to pay into Social Security and Medicare in what’s known as the Self-Employment Tax. It’s a bit of a double-whammy that catches many freelancers and gig workers off-guard. The Self-Employment tax rate is 15.3%. The rate consists of two parts: 12.4% for Social Security and 2.9% for Medicare.

You can also use Form 1040-ES (or a third-party calculator) to help you calculate your estimated Self-Employment tax and include that amount when you make your quarterly tax payments by voucher or pay online. In order to report your Social Security and Medicare taxes, you must include Schedule SE with Form 1040 when you file your annual return.

Picnic Tax, Your Accountant Matchmaker!

Now that you have a better understanding of what all goes into determining how much money you owe, you can better prepare for tax day. If you want a professional tax pro to do all the work for you so you can relax, then try Picnic Tax. Simply upload your financial documents, and our platform will match you with the perfect verified tax accountant for your unique financial situation at an upfront cost you can afford.

Click for a personalized quote to get started today!